Welcome to the thirty second in a series of articles offering insights and tips to prepare money management firms for improving their abilities to out-market competitors and attract assets from sophisticated investors in the coming post-pandemic world.

When sophisticated investors are vetting the strategies being pitched them by money management firms, performance numbers alone are not enough to win them over.

Family offices, endowments, foundations and institutional plan sponsors also look to understand where the returns came from. This is important because it helps them decide who they believe to be the skilled managers and who were simply the lucky managers.

The easier a money management firm makes it for sophisticated investors to have tangible evidence of the veracity of its investment process the great the likelihood that firm will out-market similar performing competitors that do not provide this important due diligence vetting and product differentiating information.

Clearing the muddy waters blues

While investment management firms know that sophisticated investors seek out alpha generating managers, many times portfolio managers haven’t figured out what, beyond comparing their fund returns to a benchmark, to communicate to help demonstrate alpha.

How does one figure out what a fund should focus the attention of prospective investors on performance attribution-wise?

When my financial communications and sales marketing consulting firm is brought in to help create or refine how an investment firm in its marketing can better educate and persuade prospects to understand and buy into how it invests, we delve into detailed portfolio management and risk analytics discussions with the portfolio manager relating to how she or he handles strategy implementation. In uncovering the factors that are important to the portfolio manager we many times find that some of these had not yet been shared with prospects, or even other staff members; and it was not that these were secrets. Oftentimes, it hadn’t occurred to the portfolio manager the relevance and importance of such investment considerations to outsiders who know portfolio management as well as experienced, sophisticated institutional investors and their gatekeepers do.

The factors that could find their way into performance attribution presentation data can range from effective evaluation of non-company specific risk factors to determining what to buy to how to buy it. Importantly, what are key points or prioritized elements in the investment methodology for one manager will be different from that of others.

Many portfolio managers are so close to what they do they often miss observations that sophisticated investor outsiders might note and appreciate regarding their strategy implementation. These portfolio managers can often benefit from an outside point of view in determining what performance attribution data best presents the personality and character of his or her thinking and demonstrates the veracity of the investment process used.

Here is one such example.

It never occurred to us!

My firm was tasked with helping an emerging markets debt strategy portfolio manager restructure his firm’s communications to institutional investors about the product so prospects could more easily recognize and appreciate what differentiated it from its peer group. The strategy’s performance was so good there was no trouble making it onto the short list of emerging market debt products being vetted by investment committees. However, these prospective investors had trouble differentiating this firm from others that had similar performance, and subjectively deciding whether the biggest up years, and not-as-low down years of the portfolio manager were due to luck or skill.

In our work to craft a new storyline for better educating institutional investment committee members and their gatekeepers, we deployed our process for getting out of a portfolio manager’s head points she or he hadn’t previously put into print, or properly communicated verbally, that are important elements for educating and persuading people to understand and buy into how the manager thinks and runs the strategy.

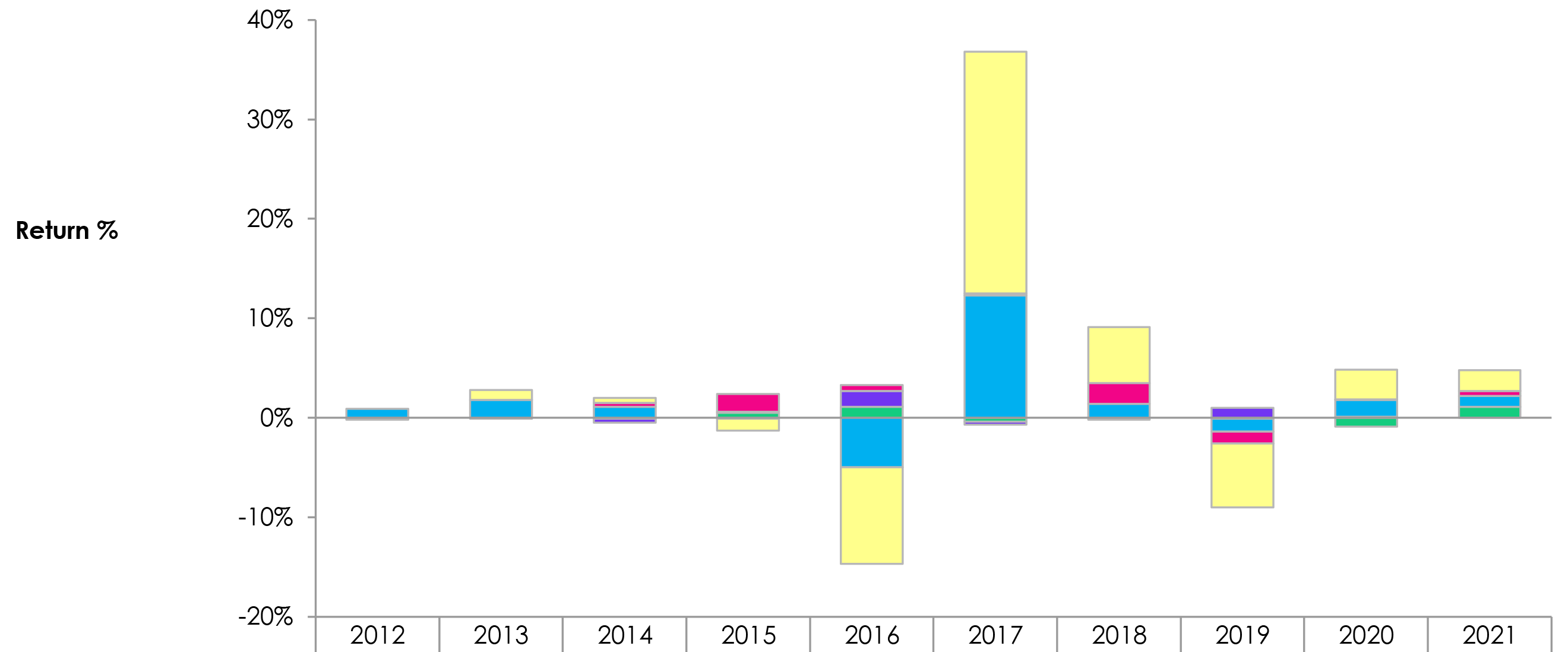

In the case of the emerging markets debt strategy portfolio manager, we determined the breakout of his investment process analytics steps and decision making that was being done. From this, we found how little of that had been communicated to prospects who had been pitched, or to the sales team. In this manager’s case, key factors contributing to each portfolio position taken were country and security selection; whether to buy in sovereign currency or USD; a duration exposure decision; and whether and how much of a cash hedge to take.

In a phone conversation with the portfolio manager to develop the new storyline to communicate how he invests, in response to a question I asked, the manager commented for the first time, You know, if we don’t get the country selection risk analysis right everything else goes to pot.

I responded that that was an important ah-ha for them to now have. Then I asked, So what does performance attribution look like on an annual returns basis when broken up by factor contribution? There was silence on the phone for about 15 seconds. I thought I’d lost our connection. Finally, the portfolio manager responded, It never occurred to us to look into that!

They ran the numbers and, sure enough, their country risk analysis turned out to be the biggest contributing factor within their investment methodology to delivering their strategy’s returns. Armed with this new data analytics, we produced a yearly returns since inception bar chart depicting the factors contributing to each year’s returns for the strategy, and had it added to the pitchbook.

When the portfolio manager and I then shared with the sales team the new storyline content created to explain both in verbal pitches and in print (but detailed in marketing collateral other than the pitchbook) about how the emerging markets debt strategy was run, we also showed them their new performance attribution flipchart page and told them how to use it at in-person meetings. With a clearer way for investment committee members to see manager skill documented, soon the firm found it was winning more new institutional allocations.

A Marketing Edge For Your Fund

To use performance attribution as a marketing edge in your money management firm’s communications and sales marketing, you must first correctly identify the relevant factors in running the strategy. Then, determine the contribution the factors play in the returns, decide how to best document and present that data in a readily understandable chart or graph, and incorporate that content in verbal presentations and written documentation about how the strategy is run.

Remember, when sophisticated institutional investors are vetting portfolio managers and their strategies, performance ranks third in importance, risk management second and investment process first. Figure out how to best use performance attribution content to demonstrate the veracity of the intellectual acumen of management in the investment process used to run your portfolio and you will have turned performance attribution into a marketing edge for your fund.

# # #